The Psycho Analyst

A creative approach to investing psychology

Follow me on X: @TheRealBirnbaum

Email me: themarket.psychoanalyst@gmail.com

Mr. Market & Madam Media

What you need to win in the markets is not what’s sold to you in the financial media. Because if they sold you what you needed, you wouldn’t need them.

Yet the market is still full up with pundits, analysts, economists, and gurus clambering to pitch you the next 10-bagger, $1,200 monthly subscription, and definitive macro indicators. Opinions are like assholes—everyone’s got one, and almost all of them are shitty.

The ones with a little integrity sell you courses on valuation, reading financial statements, calculating a DCF, calculating a reverse DCF, calculating a double-misty-backside to a front lotus DCF. And that’s all well and good, but the problem is that information and math are no more an edge than a twelve-year-old scrolling thirst-traps on his dad’s iPad. If you didn’t get that last one you either need urban dictionary or a time machine.

I’ll be the first to agree that understanding the fundamentals—knowing what you own—is essential to success. A deliberate and rigorous research process is necessary—but not sufficient. In fact, picking quality stocks isn’t even the hardest part. The statistics geeks will say, “four percent of stocks drive all the returns.” But none of us is looking at the 7,000 dogshit microcaps in the Russell. Logical actors understand that Amazon is a quality compounder. Whether they own it is another question, but in reality, I’d wager that roughly 25% of the stocks we’re actually considering are going to beat the market, and maybe 25% of those are going to crush it.

The hard part is holding these 6.25% of stocks in your portfolio in the face of irrelevant narratives and weaker quarters. The hard part is not chasing whatever’s going up and or selling whatever’s gone up. The hard part is doing absolutely nothing as Mr. Market swings to the whims of his dominatrix, Madam Media. And the hardest part of all is nailing the anaphoric climax.

Unlike Madam Media, I’m not selling you anything. My aim, pure and simple, is to help you improve your relationship with the market, your portfolio, and your goals.

But Who Even Are You?

Born and raised in the Baltimore suburbs, I spent my youth playing sports, trolling the ’hood with friends I’m close with to this day, and getting into trouble. After college I lived in Seattle for two years, where I worked as a graveyard shift concierge, and then New York for seven years, where I went to grad school for fingerpainting, stayed for the fuckery, and started working for the family business. Getting my MFA in Fiction was a terrible financial but great overall decision. It was one of the best experiences of my life. I studied with incredibly talented professors and classmates. I eventually published a novel, which I won’t link here, in the spirit of trust and an ineffable social contract that I don’t immediately try to leverage anything and everything within arm’s reach for sale.

It’s been over a decade since grad school. 37 times and counting I’ve circled the sun—or a simulation of the sun (or what I’ve been let to believe is [a simulation of] the sun). At present I’m running the family business, which I recently sold to a strategic buyer. I’m married to a Betty Draper doppelganger, which is absolutely fantastic for me. We live in Washington, D.C. with our Bernese Mountain Dog and longhaired cat. When I’m not working, I’m spending time with the girls, reading, or engaged passionately with my mistress: the market.

Here’s are more facts about me in list form, employed here to cater to the modern human’s dogshit attention span:

I’ve been an investor most of my life. I used my bar mitzvah cash to buy my first stock at age 13 ($IBM), which I held for almost 20 years. I bought my second and third stocks at age 29 ($TEVA and $S, now $TMUS). For reasons that will become clear over time, I took a fully active approach at age 31. Through a combination of stocks, real estate, turning around and selling a business, and marrying a whip-smart woman with a decent federal retirement portfolio, I’ve roughly 300X’d my net worth since buying IBM—a 26.83% compounded annual rate for my good house. I’ve only been accurately tracking my time-weighted returns for two years, which results I will share as well.

I’m a CEO—for now. I led the sale of the family business about a year ago. Integrating with the acquiring company means I’ll eventually be demoted to Managing Director. Once integrated, the idea is that I’ll become more of an account manager and closer of our biggest clients and prospective biggest clients. Or maybe I’ll be laid off so they can increase margins. Anything can happen.

I’m a former sports junkie and actual recovered junkie. I belabored the decision over whether to share this information. For one, I can’t imagine what my dad will think when he learns I’ve stopped watching Yankees games. And then of course there’s my former drug habit and multiple overdoses. Jokes aside, addiction has played a huge role in my life. I’ve been hooked on videogames, sugar, Back to the Future (for a year circa age six), snowstorms (I’m serious), cigarettes, cereal, and, of course, the market. Addiction has both ruined and saved my life. Other than squelching out the stigma, I choose to discuss addiction early and often because my personal, portfolio, and market analysis would otherwise be disingenuous. I got clean six years ago—just months before I rolled over my 401K and began running my own money.

I’m a CODA. If you haven’t seen the movie, which won Best Picture, CODA stands for child of Deaf adults. In case you can’t parse this eerie prepositional phrasing—which is a little to “of the corn” for my taste—this means both of my parents are Deaf. I use a capital D because they’re culturally Deaf and use American Sign Language, rather than simply afflicted by hearing loss. ASL was my first language, but my game got weak because my parents constantly spoke to me.

Despite my Irish given name, I’m a Jew. I didn’t want to mislead the antisemites, who have, are, and will always be everywhere, and can now make a graceful and anonymous exit.

About being a former sports junkie—I played baseball and basketball at a high level. Especially the former. I played shortstop and batted anywhere in the first four slots on the metro team. In high school I developed a brutal case of the yips. If you know about Chuck Knoblauch or have read The Art of Fielding, you know what I mean. By junior year I’d quit everything. This triggered what is a congenital miasma of psychological pathologies—namely depression, OCD, and addiction, a Russian nesting doll of mental maladies whose final little babushka at center was my tendency to self-medicate. I catch the Yankees during the playoffs.

I majored in finance and psychology at the University of Maryland—which perhaps qualifies me to practice market psychoanalysis. I should admit: during fall midterms of junior year I quite literally forgot to show up for an exam. (I was actually a pretty good student, despite my attendance rate. I was the Tampa Bay Rays of college. Four years of all As and Bs were ruined only by my D in Jewish Studies. I was otherwise subject-agnostic.) Back then I took the easy way out whenever possible. Rather than trying to fix it with my professor with an excuse, I changed course entirely and switched majors to psychology. It was one of those situations analogous to the effort put into cheating on a paper surmounts that which would have been required to write it straight up. Furthermore, I tried to donate my slot at UMD’s Smith School of Business to my roommate, who was trying to get in as a junior. Unfortunately, my guidance counselor declined to entertain my last b-school act of benevolence.

I actually underwent psychoanalysis for three years. Shortly after these three years I ended up in rehab. You might reach the not unreasonable conclusion that the analysis didn’t take. On the contrary, it took all too well. By the end of those three years I was unable any longer to compartmentalize the facts, namely that: I loved but was not in love with my girlfriend—and best friend; the novel I’d been working on for five years and had once been represented by a major literary agency was not going to achieve major publication; my relationship with substances, improved dramatically during the first year of analysis, had devolved to a stark dichotomy—either I was going to stop, or embrace degeneracy with reckless abandon. Over time, I’ll unpack my experience with analysis. To say it “failed” would be a gross oversimplification. Few things allow one to stretch the limits of cognitive exploration—lying supine five days a week, doing nothing but thinking and talking about your thoughts, memories, feelings, beliefs, resentments, worldview, diet, desires. It also at times blends into mental masturbation, and I found my analyst’s dogmatic adherence to the silent treatment to be deeply corrosive over time. Taking the role as market psycho analyst, my position is diametrically opposed.

It’s easy for us to tell what’s wrong with other people. Analysis is a method of getting someone to talk themselves into awareness. Despite investors’ different strategies, goals, ages, locations, we’re all basically trying to achieve the same things. Call it retirement, financial independence, Fat FIRE—it’s all a variation of freedom. The patient talks, and the analyst listens. Whether I’m the former and you’re the latter is almost irrelevant. The experience is therapeutic for the psychoanalyst as well.

Every week, day, month—whenever I feel like publishing—I will share my buys, sells, thoughts on the market, feelings about a given management team, industry analysis, business model preferences, economic prejudices, experiences with investing or life writ large—whatever I feel like sharing. Maybe you’ll email me your thoughts, questions, and sentiments. Maybe you’ll start writing yours down for yourself or starting your own Substack. Either way, by merely reading what I write, we’ll all discover something about ourselves and the way we invest.

At times it will be uncomfortable, like when you discover a family member you’ve always liked and even occasionally text for non-logistical reasons has been cheating on their spouse with their spouse’s sibling. You don’t want to [sell]. You really like [the company]. You like spending [the money you make from the company’s stock]. But you also know that, at some point, the [fundamentals] will eventually [take over the stock price].

There’s probably a personality test to be found by replacing the brackets with narrative-appropriate terms.

Let Them Eat Cake

If at least to prove that this is in fact a markets-focused digital record, I’ll leave you all with one last thing: a rough calculation of my net worth and brief review of my portfolio.

Net Worth

Psychoanalysis requires comprehensive transparency. Analyzing our approach to the market requires analyzing our lives.

This includes my portfolio and, even more important, financial context.

As we’ll discuss next time when we analyze the alleged AI “bubble”, an assessment of value requires context. My age, marital status, portfolio, job and career, and net worth mean nothing without each other.

Everyone on Earth knows the net worth of Elon Musk, Jeff Bezos, and Larry Ellison. We obfuscate our personal circumstances out of propriety, and somewhat for good reason. Some of us don’t want our friends to see us differently. Don’t want family asking for money. Don’t want employers or prospective partners to know our level of indebtedness.

But that’s some of us. Personally, I believe that dissembling our financial condition has for the most part worked to our detriment as a society. Untold millions have lived entire lives—hundreds more are currently living their lives—without a complete understanding of money, how it works, and how it should be managed.

For our purposes, it’s more pointed. Psychoanalysis requires comprehensive transparency. Analyzing our approach to the market requires analyzing our net worth, portfolio, and goals.

Real estate investments:

· Apartment 1: $36,500 equity (owned since March 2022; renting out at cost of mortgage, HOA, taxes, and insurance)

· Apartment 2: $178,100 equity (owned since March 2025; current residence)

· Series of investments in syndicated trust run by orthodox Jews whom we met through our Deaf rabbi ($225,000 equity, blended average dividend of roughly 8% thrown off into stocks)

Retirement plans:

· My Roth 401K: $44,250 (index funds)

· Wife’s federal TSP: $155,000 (index funds; also, this is really $185,000 but we borrowed against it to renovate our kitchen with a payback plan of three years)

Net Worth:

$634,000 (all of the above) + $1.279m (Schwab, as of close on December 12)

= $1.917m

Not bad for a prodigal son with a rap sheet and extended stint in rehab. (Seriously, they were worried about me. I was in detox for 24 days.)

Portfolio

In another demonstration of my integrity, I’ve screen-grabbed my portfolio on one of the poorer trading sessions of the year. I’m still getting used to the occasional $50,000+ swing in my portfolio. First-world problems.

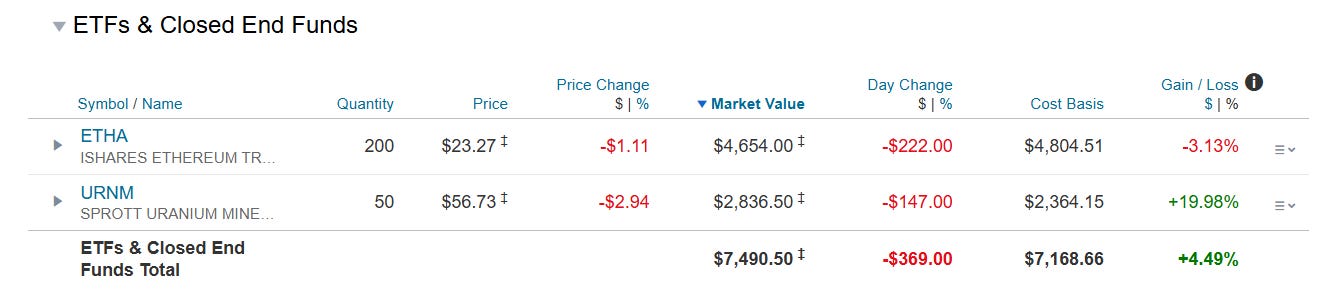

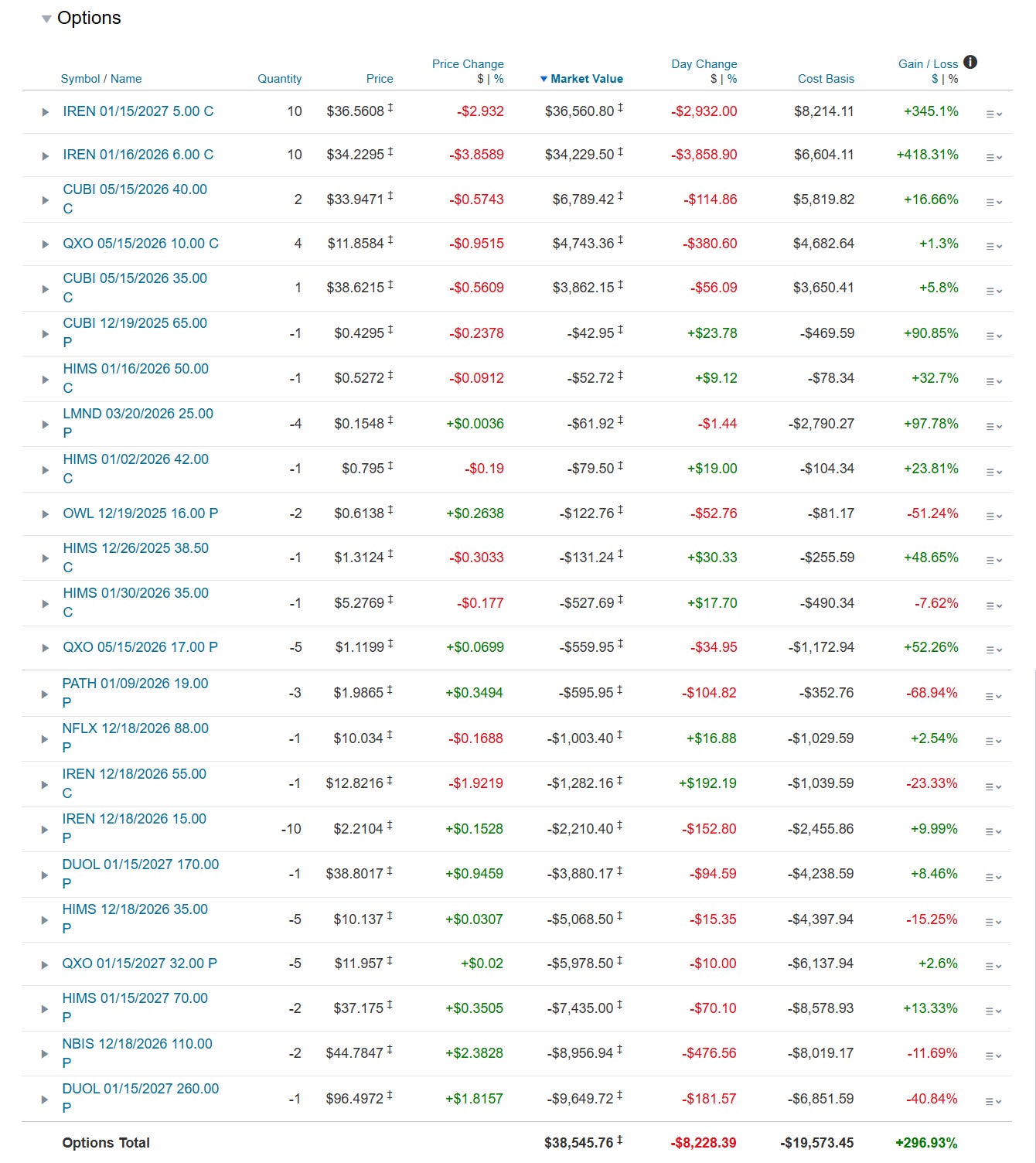

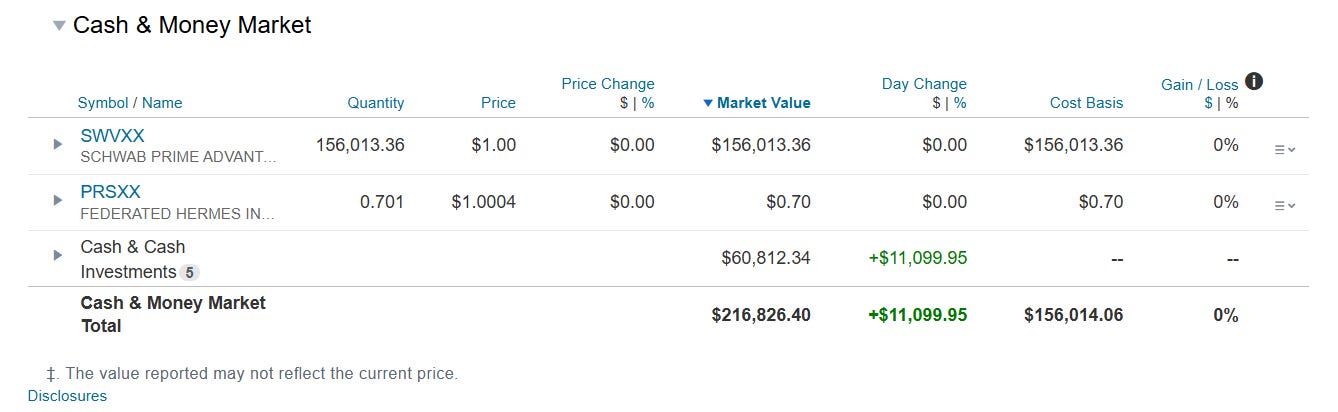

The following shots are cordoned between:

Equities

ETFs

Options

Cash & Equivalents

All holdings are abstracted across my accounts—i.e. IRA, Roth, HSA, etc. Not included are our workplace retirement accounts—i.e. 401K and TSP.

Equities

The most salient features of my stock portfolio are:

I own 24 stocks.

My top five holdings make up nearly 47% of my portfolio (and that includes ETFs, options, and cash; but doesn’t include nominal potential exposure to short puts). Note that $IREN, not $HIMS, is my fifth largest position; nearly the whole of my position is through deep ITM calls.

I favor capital-lite businesses that don’t need to reinvest much cash for growth. Namely tech and financials. Subthemes mark the differences, such as serial-acquirers Kelly Partners Group (OTC ticker $KPGHF) and $QXO, but even these fall firmly within the umbrella mission. I favor businesses whose value rides on the backs of world-class management teams and talented people. These businesses inevitably build the best technologies, develop the most efficient business models, and hire the most talented people.

If I’d sold the business two years earlier, I’d be much closer to my goals. When I first bought $PLTR, it was between 8%-10% of my portfolio. Not only would the position be many times bigger, but I also believe Palantir isn’t close to reaching its full potential. Salesforce was trading at a similar multiple in the aughts. Investors always have and always will engage in hyperbolic discounting, and Palantir is one of the best businesses in history. The remainder of my portfolio would of course be much higher as well. Then again, at that time Dollar General ($DG) was one of my biggest positions.

The most recent buys are $PATH, $OWL, and $NFLX. I also bought $ADBE but sold within days because of the rapidly developing opportunity in $NFLX. The vast majority of my “trades” are small initial positions such as these.

I buy a sub-1% position for a gut-check. Ideas alone can’t make contact with conviction; money is the chemical that jumps the synaptic cleft. Sometimes it takes months, others just days, to really understand how I feel.

Anyone who says feelings play no role in fundamental analysis is either lying or doesn’t understand the human condition. Conviction is a feeling. Every aspect of our judgment and analysis depends, anatomically, biologically, on feeling. It’s no wonder that we tend to make better decisions when we’re calm and positive. We tend to make poor decisions when upset or anxious, particularly in a state of panic. Selling stock on days like Friday is almost always a bad decision.

Generally speaking, the larger the position, the longer it’s been in the portfolio. This is by design. I buy stocks with the intention of holding them forever. While a company’s performance over the long run rarely warrants permanent ownership, you only need a handful that do to achieve market-beating returns. In fact it’s the same premise as the market; except, instead of spreading my bets across 500 companies, I’m confident that I can find a few across 25.

I do not hedge, rebalance, trim, etc. I invest. The company that bought our business last year doesn’t have any intention of trimming pieces of ownership or rebalancing them against other interests. You don’t trade around a farm. Stock price gyrations are meaningless outside the opportunities they give me. Their value is measured against a far more metaphysical reference point than 99.9% of market participants realize, to their detriment: time.

Investments are a wager that time will allow a business to realize its value. The ability of an investor to understand a dynamic world, from general themes to granular developments, decides her success. The investor must see a future, place her bets, and wait patiently as that future is made manifest. This is the essence of my process.

ETFs

The most salient feature of my ETF portfolio is the tiny allocation. I prefer concentrated investments in businesses. However, when I see a broad macro trend or opportunity, I’ll act. I believe in Ethereum’s gas fees and the outsized effect nuclear will play in bridging our energy needs from fossil fuels to renewables. The latter will take time, and I want to be early.

Options

The most salient features of my stock portfolio are:

A few of my positions are loaded up as deep in-the-money (ITM) long calls. For the uninitiated, ITM calls allow me to control 100 shares of stock at a fraction of the price. Further, if I pair it with a cash-secured put (CSP), I can cancel out the small premium I’m paying for the call. I control all or most of my interest via deep ITM long calls in $IREN and $CUBI.

I use CSPs heavily to purchase more stock and/or juice returns. This is a heads I win tails you lose situation. Either I buy the stock for lower than its price when I wrote the put, or the stock price remains higher than the CDP strike, and I keep the premium.

I also use covered calls (CCs), albeit more tactically. The last thing I want is to allow shares that have been compounding to be assigned in the midst of a huge run. I’ve seen investors get caught in the death spiral of frantically rolling the calls higher, requiring longer and longer expiration dates, thus raising the probability that they will again need to roll. I use CCs either:

to sell stock and raise cash for other purchases

or way out of the money for small premiums

The latter I seldom deploy for fear of the death spiral. Investors mistakenly believe the biggest risk to be losing money—especially because of Buffett’s rules one and two. This is misguided. The math is clear. By an asymmetrical margin, the biggest mistake you can make is selling a winner.

I also use deep ITM short puts as a sort of reverse deep ITM long call. The idea here is the same exposure to a stock, only with a capped gain, but with the benefit of getting a lump of cash to reinvest, typically in the same stock. With long expiration dates, the best case scenario would be the stock price rising to just short of the strike so I’d retain all shares and avoid any tax on the premium until I sell them.

Most recently, I wrote put options for $PATH, $OWL, and $NFLX.

Cash & Cash Equivalents

The most salient features of my cash and cash equivalents are:

The nominal ~16% of my portfolio in cash is a real ~5%-7%. I’ve created a personalized formula for weighing the probability of options obligations I will need to meet. The formula is quite conservative, proven by the consistent overestimation of actual vs. predicted obligation.

Despite the data, I prefer to have some cash on hand for times of market distress. The gains I’ve realized from $HOOD and $LMND have come purely from the Liberation Day fiasco. I was lucky enough to have bought these stocks near their April lows.

I keep as much cash as possible in money market (MM) funds. I’m more than happy to buy stock on margin and sell down my MM to cover the cost. 3.5% yields $7,000 a year against $200,000. This past week we moved another $40,000 to Schwab, which was a portion of our first earnout from the sale of the business. I will be purchasing MM shares in the coming days depending on how much stock I buy during this dip.

Goals

My goal is the same as everyone’s: freedom. Money doesn’t buy happiness, but it buys freedom, which gets you pretty damn close.

At no point do I wish to “retire” in the conventional sense. I can envision a happy life waking up, brewing coffee, and reading, spending time with the girls, traveling, seeing friends and family. And I might even be truly happy.

But I wouldn’t be fulfilled.

Happiness isn’t overrated, but it is ephemeral. Pursuing happiness is like pursuing a championship. You’re just going to want another one.

Fulfillment lies largely in the attainment of goals, and goals are like Russian nesting dolls. Within pursuit of freedom lies the pursuit of passions, within which lies the pursuit of achievement within those passions.

Fulfillment, like most things, is fractal. There are infinite shapes of it within it. By pursuing freedom, I pursue them all.

Post Dos

There’s no formula here. I don’t know what the next post will bring. But I do know three things we’ll review:

The AI “bubble”

My 2024 and YTD 2025 performance, along with discussion of my performance in years prior to when I began tracking my performance.

How bad an investor I was when I started.

All changes to the portfolio since the previous post—which will continue with each post.

A more granular review of my holdings.

A more detailed discussion of Madam Media—and her stranglehold on Mr. Market

Till then.

Excellent 👌